Rescheduling Makes Cannabis Business Lending More Attractive

What DEA rescheduling means for cannabis business lending

For the better part of a decade, cannabis lending has been a math problem. Even profitable operators couldn’t fit under conventional lending criteria. Not because the businesses were bad, but because IRS Section 280E was systematically destroying the cash flow lenders rely on to underwrite credit.

That problem just got materially smaller.

On April 22, 2026, the DEA finalized the move of FDA-approved products containing marijuana and marijuana subject to state-license, from Schedule I to Schedule III. Adult-use, synthetic THC, and unlicensed bulk product remain Schedule I. The reshuffling is narrow, but for the slice of the industry it touches, the lending math flips overnight.

280E was a lending killer

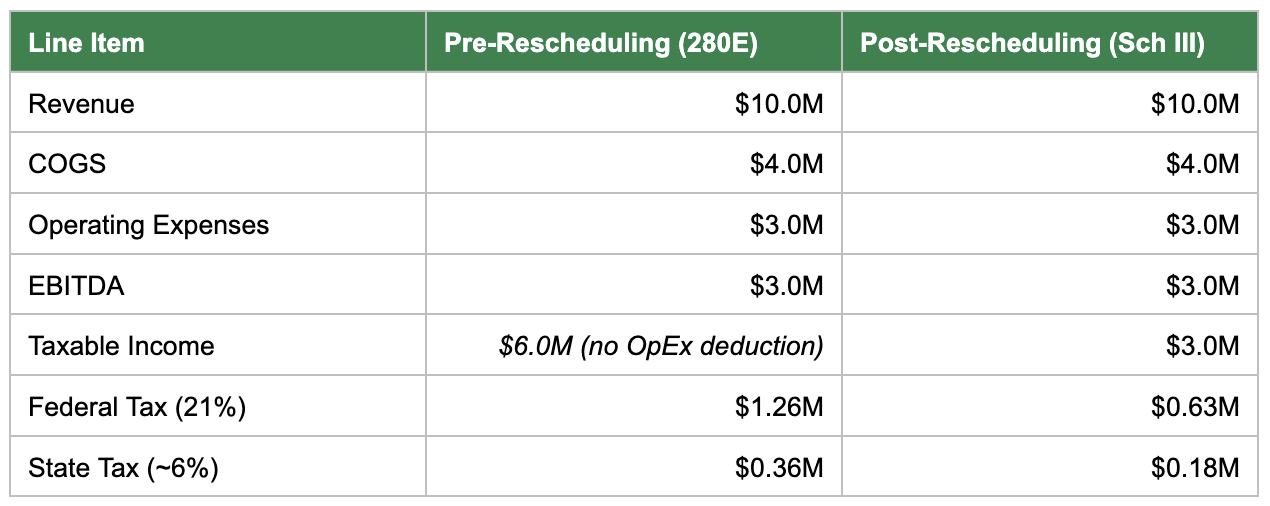

Under 280E, cannabis businesses can deduct cost of goods sold but not ordinary business expenses. This means no deductions for rent, payroll, marketing, professional fees, etc. The result: they pay federal tax on gross profit instead of net profit. Effective tax rates routinely hit 60–80%, sometimes higher.

That tax burden doesn’t just hurt margins. It vaporizes the cash flow available to service debt.

Schedule III substances aren’t subject to 280E. Medical cannabis operations now under Schedule III are able to take the same deduction treatment as any other business. The federal industry savings are estimated at ~$2B annually.

What this looks like on a real operator

Consider a $10M-revenue medical cannabis operator with typical industry economics:

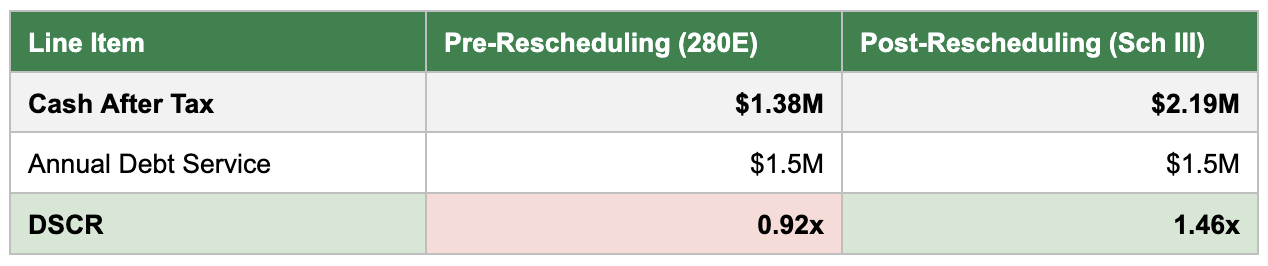

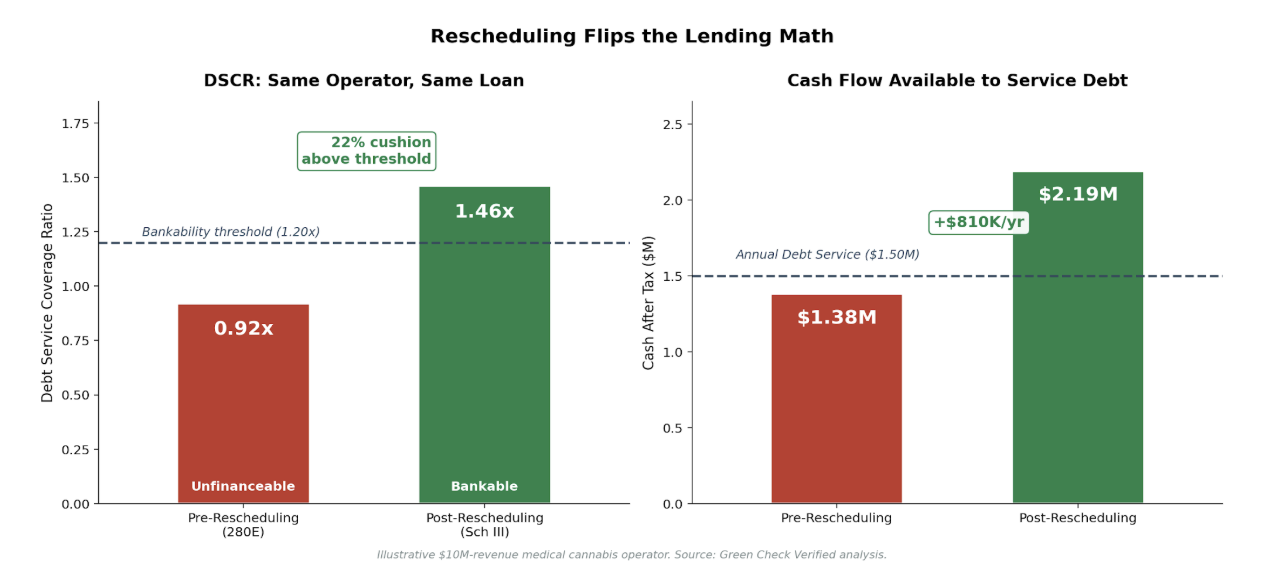

Same business, same operations, same loan. The DSCR moves from unfinanceable to comfortably bankable.

Figure 1. Same operator, same loan: rescheduling moves DSCR from unfinanceable to comfortably bankable.

Why DSCR matters

DSCR — net operating income divided by debt service — is the single most important number in commercial lending. Most lenders won’t touch a deal under 1.20x. SBA underwriting typically requires 1.25x. Conservative lenders often want 1.35x or higher.

Pre-rescheduling, the operator above couldn’t service their loan, full stop. The lender was looking at a borrower who appeared profitable on paper but couldn’t actually make the payment after the IRS took its cut.

Post-rescheduling, that same operator has $810K of additional annual cash flow which is enough to clear the bankability threshold with a ~22% cushion. That’s not an edge case. That’s the new baseline for medical operators across the country.

For FIs that have stayed on the sidelines because the credits didn’t work, the credits now work. The deals you turned down 18 months ago deserve a second look.

Federal oversight reduces lender risk

Schedule III isn’t free. Medical operators must register with the DEA, pay the $794 fee, comply with federal storage and recordkeeping requirements, and submit to inspections. The expedited 60-day registration window opened April 29, 2026.

For operators, this is a new compliance burden. For lenders, it’s a feature, not a bug.

DEA registration creates a federal regulatory touchpoint that didn’t exist before. It produces standardized inventory data, mandatory reporting, and inspection authority, all of which raise the floor on operator quality and reduce the kind of “rogue operator” risk that has historically scared institutional capital. Lending into a federally-registered, federally-inspected business is much closer to lending into a pharmaceutical distributor than into an non-federally-regulated state-legal dispensary.

Of course, that same compliance surface area also creates new monitoring obligations for the FI itself. FIs will need to identify which businesses (or individual business lines within a mixed-use license) are Schedule III, which are Schedule I, which operators are properly registered, and how that changes risk weighting and monitoring. Most FIs aren’t built to track this on their own. Specialized platforms matter more now, not less.

Bankruptcy protection: the open question

Here’s a wrinkle that hasn’t received enough attention. Federal bankruptcy courts have historically refused to grant relief to cannabis businesses on the grounds that the underlying activity violates federal law. That meant lenders in trouble had no clean Chapter 11 or Chapter 7 path and they were stuck with state-level receiverships and informal workouts.

Schedule III may change this for federally-registered medical operators. The legal theory that bankruptcy protection should be denied because the business is federally illegal weakens considerably when the business is a federally-registered, DEA-overseen Schedule III operator.

This is unsettled. It will be tested in courts over the next 12–24 months, and outcomes may vary by jurisdiction before a circuit-level consensus emerges. But even the option value of bankruptcy protection materially improves the workout calculus for lenders. Loss-given-default estimates, recovery scenarios, and intercreditor arrangements all look different when Chapter 11 is on the table.

Mixed-use operators benefit too

A lot of the public conversation has framed rescheduling as a pure-play medical event. That misses the bigger picture.

Most operators in mature cannabis markets are mixed-use, meaning they offer medical and adult-use cannabis under the same roof (and often the same brand). Those operators are not excluded from the benefit. They will likely register their medical activities under Schedule III to capture the 280E relief on that portion of the business. Adult-use lines remain Schedule I, but the medical books get the clean tax treatment.

The IRS still has to issue apportionment guidance so the industry understands how to properly split costs between Schedule III medical lines and Schedule I adult-use lines. That guidance is forthcoming (DOJ’s April 23 release confirmed it’s in the queue, which was later confirmed the same day by the Treasury Department). When it lands, the math will be more complex but the direction is clear: any operator with a medical license benefits, even if they also run adult-use.

For lenders, this means the addressable financeable market is significantly larger than the count of medical-only licensees suggests. The collateral pool for any mixed operator now contains a Schedule III sub-business with materially better unit economics.

What FIs should do this quarter

The 60–90 day window after a shift like this is when relationships are won. Operators who couldn’t get a credit conversation in March are now looking for capital partners. The first FIs to update underwriting models, re-train credit teams on the new tax math, and proactively reach out to their cannabis-banked customers will capture the relationship value.

The deals you couldn’t make work last quarter? Run the numbers again. The DSCR may have moved a full point.

Reach out to Green Check with any questions your institution has on rescheduling.