The Indirect Cannabis Opportunity

When financial institutions make the decision to offer services to the marijuana industry, they naturally look at the market opportunity to determine whether the effort associated with the increased compliance obligations is outweighed by the potential benefits. Compelling numbers from media outlets like Flowhub that marijuana sales nationally will exceed $32 billion in 2022 often prompt financial institutions to start looking into cannabis banking, but there are limitations that can lead some banks and credit unions to rethink their decision once they start looking deeper at the opportunity, like caps on the total number of licenses available or a perception that all of their local marijuana businesses are already banked. But it’s important to understand that the true cannabis market opportunity extends far past marijuana itself, and in even the most restrictive states there is an ever-growing number of cannabis-related businesses that don’t “touch the plant”.

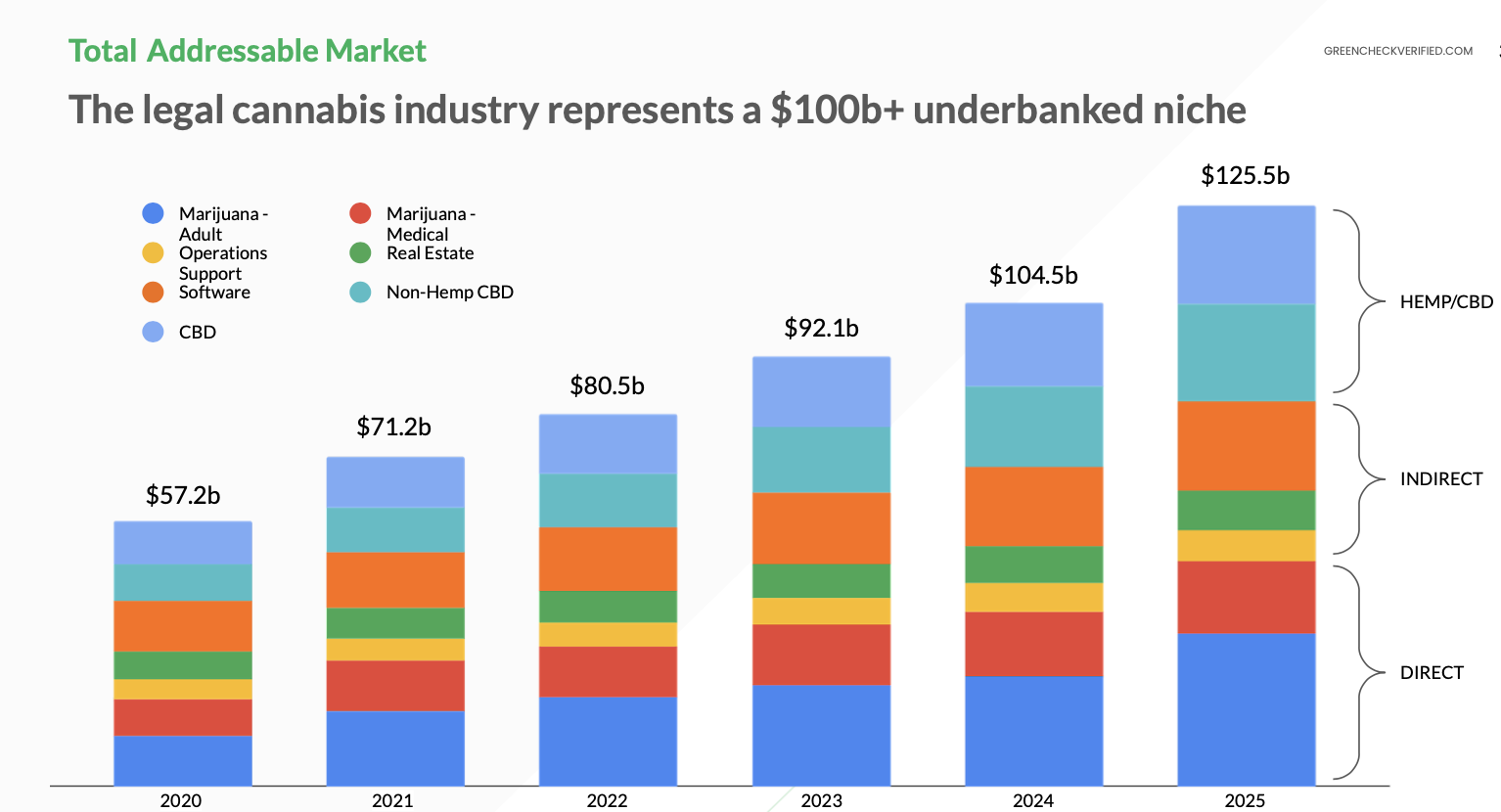

When analysts describe the market opportunity presented by cannabis they’re myopic in their outlook, focusing on those licensed by a state or territory’s cannabis regulatory authority (aka “plant touching”), known as Direct Marijuana-Related Businesses or “Direct MRBs”. The reality is that Direct MRBs are only a small piece of the cannabis puzzle. Beyond these Direct MRBs there are also what we call Indirect Marijuana-Related Businesses, i.e. those that derive a significant portion of their revenue from Direct MRBs. These present a lower level of risk because they do not work with a federally controlled substance, but they do derive a significant portion of their revenue from them.

Additionally, it’s important to remember that cannabis isn’t just marijuana. Even though hemp is federally legal, it still looks, grows, and smells like its cousin marijuana. The difference ultimately comes down to the result of a laboratory test: when cannabis contains less than 0.3% of the chemical delta-9 tetrahydrocannabinol (THC) it is legally hemp, and when in excess it is marijuana. Consequently, there is risk associated with hemp because of its close relationship with marijuana and The Department of Treasury’s Financial Crime Enforcement Network (FinCEN) accordingly released a guidance document in 2020 that lays out specific compliance regulations to reflect it. Lastly, there are businesses that focus on the sale of hemp-derived products, notably of cannabinoids like cannabidiol (CBD) that you can find in gummies available online and in major national grocery stores and pharmacies.

Evaluating the size and opportunity of the Direct MRB market is relatively straightforward compared to Indirect, Hemp, and CBD businesses because they are so highly regulated. The entire marijuana supply chain from the moment a seed is planted in the ground all the way through to a retail or medical sale is tracked and reported to the state or territorial marijuana regulatory authority, so comprehensive sales data does exist and most states or territories share it publicly to some extent. Therefore, analysts can build reliable models to quantify it. However, as there is no consistency in how Indirect, Hemp, and CBD businesses are tracked or licensed across the country, there’s no easy way to get that information. With no existing model available for quantifying the Indirect, Hemp, and CBD market, it’s understandable that pundits effectively ignore it, but to do so tremendously underestimates the size of the opportunity available to those that are ready to bank cannabis businesses.

Starting with Indirect MRBs, to estimate the size of the market one has to take the definition of these businesses – those that derive a significant portion of their revenue from Direct MRBs, often 51% and above – and look at the kind of businesses that would fall into that bucket. The examples that most readily spring to mind are the lawyers, accountants, electricians, plumbers, and other tradespersons that service the industry daily as well as the landlord or property owners that rent to Direct MRBs. This highlights one of the fundamental challenges inherent in defining this opportunity – a lack of publicly available information about revenue derived from providing professional services to the industry. However, when widening the aperture beyond these industries, there are often other kinds of businesses that do make some of that information available to those ready to do detective work. It’s not a straightforward process, but through figures shared in the news, via press releases, or disclosures made by publicly-traded companies that service the industry, a picture begins to form.

Based on our research, we’ve been able to pull together figures for some of the businesses that fall into the Indirect MRB category in the areas of Operations Support, Real Estate, and Software. In each of these categories we’ve collected as much verifiable information as possible, with the caveat always being that the data set will always be somewhat incomplete because many cannabis companies keep their revenue figures close to the vest.

Under Operations Support, we looked at companies like testing labs, product packaging and industrial equipment manufacturers, lighting companies, insurance providers, PR and marketing forms, electronic payment solutions, and cash transportation vendors. Based on available data, this category adds at least $9 billion on top of the Direct MRB opportunity. Under Real Estate, we collected as much information as we could around those companies that provide retail, processing, and agricultural space to Direct MRBs, as well as a popular vehicle for financing Direct MRBs that need access to capital that can’t get it through traditional banking relationships, the Real Estate Investment Trust or REIT. That adds $6.5 billion to the total. Software includes firms that provide point of sale software to MRBs, seed to sale tracking software to states and territories, payroll and HR services, and supply chain management software among others, adding $12 billion. That puts the Indirect MRB opportunity at just under $28 billion, comparable to the figures often cited for the total marijuana opportunity in the country.

Hemp figures vary wildly based on the source, but through information we’ve sourced we estimate that the market for agricultural or industrial hemp, based on revenues from the sale of fibers, textiles, seed, meal, and oils, is $21 billion. Adding in sales data for CBD sales in general retail (online and brick and mortar), pharmacies, and marijuana dispensaries are around $18 billion, making the combined hemp and CBD market worth approximately $39 billion dollars, outpacing the estimates for Direct and Indirect MRBs respectively.

We consider our figures to be incredibly conservative based on our decision not to include figures that we couldn’t tie back to a reliable source, and it’s clear that marijuana only represents about a third of a $100 billion cannabis market. There is a tremendous opportunity available to financial institutions in states with hard license caps like Utah and Ohio, in states and territories where sales have yet to begin like Alabama and Virginia, in states that have yet to legalize marijuana like South Carolina, or even for those banks and credit unions that aren’t yet ready to take on Direct MRBs.