How To Use Deposit Data For Cannabis Banking Success

Cannabis banking data is the ticket to building a successful and profitable program.

If you operate a cannabis banking program or are thinking about launching one, gathering and tracking data is critical. From both a business and compliance perspective, you can’t get very far without concrete numbers to back up your expectations. However, with strong data in your corner, you’ll be well positioned to succeed. This guide explains the importance of data and how Green Check can pull the curtain back on the cannabis banking space so your financial institution can operate from a competitive advantage.

Why is cannabis deposit data important?

In cannabis banking, deposit data is important for both monitoring and compliance purposes, as well as the success of your financial institution in the space.

When it comes to ensuring you meet your anti-money laundering (AML) obligations under the Bank Secrecy Act (BSA), tracking deposit data on the individual customer level is essential. Anomalous deposits or deposits that don’t match up with sales data could be worth flagging and investigating. That could warrant the filing of a suspicious activity report (SAR) with the Financial Crimes Enforcement Network (FinCEN).

On a broader level, understanding what types of deposit data are typical for the industry and, more importantly, your market, can help you determine whether your cannabis banking program is succeeding. Even before you launch your cannabis banking program, you can leverage industry-wide deposit data to determine if the opportunity is big enough to justify the costs of entering the cannabis space.

Are you a cannabis business owner interested in using data to grow your business? Check out our guide on how cannabis businesses can use data to improve operations.

How to use deposit data for your cannabis banking program

Deposit data and the associated data that comes along with it can be useful to financial institutions in a number of ways. Here are some of the most important ways to make cannabis banking data work for you.

1. Determine whether a cannabis banking program may be profitable

If you haven’t yet launched a cannabis banking program but are considering doing so, you’ll want to do enough research to understand whether there’s a profitable opportunity. One of the best ways to do so is by reviewing the deposit data of CRBs in your market. This data not only shows you how much deposit activity is occurring in the space, but what types and how profitable that activity may be.

For instance, if your market is seeing a lot of low-cost organic deposits, there’s a big opportunity to generate a return by lending those dollars out. On the other hand, if other financial institutions in your market are drawing deposits with higher cost Certificates of Deposit (CDs), the opportunity to generate a return may be lower. Data can help you better understand this before you invest in launching a program.

2. Conduct ongoing monitoring of CRB accounts

Once you decide to work with cannabis businesses, you become responsible for the ongoing monitoring of their accounts for KYC and AML purposes. Fortunately, you don’t need to reinvent the wheel; the 2014 FinCEN guidance sets a clear foundation for how to work with cannabis businesses. Tracking their sales and deposit activity is a major part of this, as anomalous activity can be a signal of bad behavior. By understanding typical sales and deposit data in your market, as well as typical sales and deposit data for your individual customers, you can easily spot these red flags should they crop up and take the necessary action for your cannabis banking program to remain compliant.

3. Track cannabis banking performance over time

Whether presenting to the board or just tracking the day-to-day performance of your cannabis banking program, data is a critical element. You can use these numbers to track against expectations and ensure your program is growing at the rate you need it to. For example, if you open a cannabis banking program in Connecticut with the goal of opening five accounts per month and attracting a certain amount in deposits from cannabis sales and retaining a certain percentage of those deposits over time, this data can help you gauge your success.

Further, by drilling down into your own data, you can keep tabs on your balance sheet and ensure you maintain the appropriate deposit mix for stability and profitability. If deposit levels increase too much, you can easily flag that to slow the opening of new accounts or begin issuing more loans. If new deposits are primarily coming in the form of CDs, you can make sure you’re offering attractive terms in your market while making a push to bring in more organic deposits through business checking accounts. Without access to detailed data and context as to what’s going on in the market, this type of nimble adaptability becomes difficult. Having access to this data gives you a competitive advantage.

How Green Check provides robust deposit data

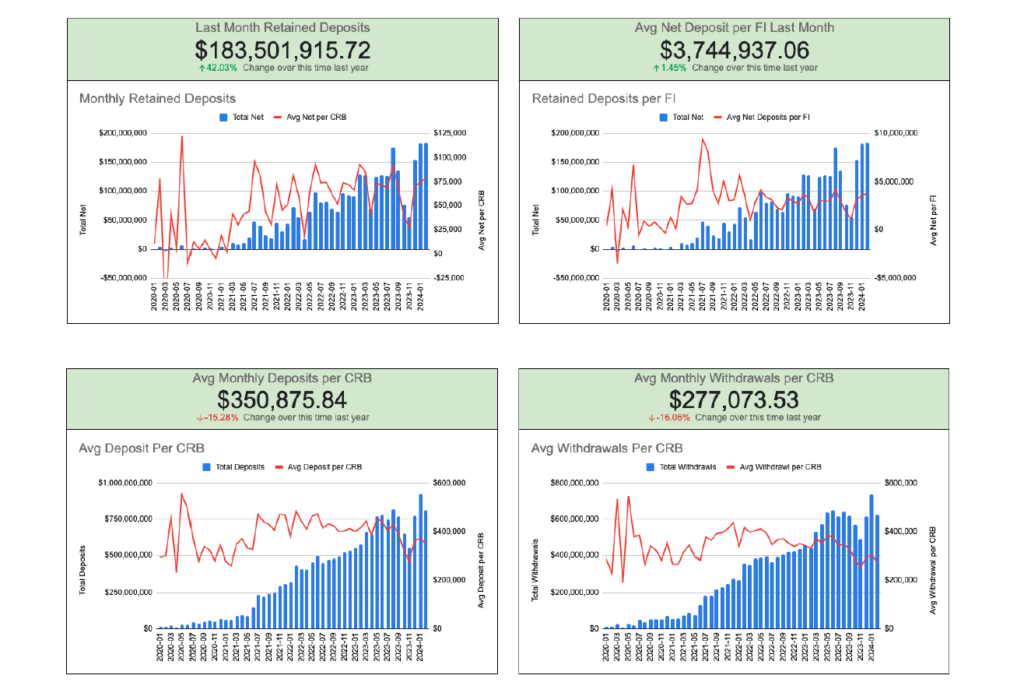

Green Check compiles cannabis banking data from over 100 financial institutions operating in the space and the thousands of cannabis businesses they work with. That means, through the Green Check Verified dashboard, you can gain strong insights into the current landscape of cannabis banking, including deposit and withdrawal patterns of CRBs, sales data, and more.

With Green Check Verified, you can get a clear picture into the cannabis banking space. This information helps you determine the right time to launch a cannabis banking program, tailor your program to the needs of your customer, and conduct the legally required monitoring that comes along with banking cannabis businesses.

Here’s a quick snapshot of just some of the data Green Check Verified makes available to financial institutions:

- Banked CRBs: Understanding how many CRBs in your market already have a bank versus how many licensed operators exist in your market is an indicator of how much opportunity remains. If the number of banked CRBs is much lower than licensed operators, you’ll have a good chance of attracting some customers when you launch your cannabis banking program.

- CRBs awaiting approval: Understanding how many CRBs are awaiting licensing can also paint a picture of your market’s near-term growth prospects. If a lot of businesses are in line for licenses, they’ll likely need banking soon enough. You can use this data to target cannabis businesses that will soon come online to bring them into your portfolio and bolster your program.

- Sales data: Detailed sales data by day, week, and month can help you understand the typical patterns of a CRB in your market. This can help you forecast the deposits that are likely to come into your institution and plan accordingly on how to lend those dollars out. Tracking sales data is also important for compliance monitoring; while some fluctuation is to be expected, any major spikes or dips could be reason to take a closer look at these accounts, helping you stay compliant with federal regulations that apply to cannabis banking.

- Sales vs. deposit data: In the legal cannabis space, it’s fairly common for businesses to withhold some cash and only deposit a portion of their sales. Even though some of those dollars may never enter your financial institution, it’s important to track this behavior. If there’s a sudden shift in the amount of cash being withheld, for example, it could be a signal that something suspicious is happening — and it’s your responsibility to file an SAR with FinCEN as a result.

Build a better cannabis banking program with Green Check

In cannabis banking, data is king. Fortunately for your financial institution, Green Check Verified provides the keys to the kingdom. When you want to know more about cannabis banking nationwide or at the state level, Green Check is the best source of information around. Don’t enter the cannabis banking space without the support of industry experts. At Green Check, we make starting, running, and growing a cannabis banking program as seamless as possible — contact us to learn more about how we do it today.